The Sabka Bima Sabki Raksha (Amendment of Insurance Laws) Act, 2025, was introduced by the Government of India with the objective of ‘insurance for all’. The new amendment is going to reverse the traditional insurance landscape in India. It allows private and foreign investors to step into the insurance ecosystem, which has historically relied on public welfare institutions. The shift is quite pivotal as the existing insurance system in India relies on large state-funded schemes such as Ayushman Bharat (PM-JAY).

The new entrants to the industry can provide attractive policies and opportunities in the insurance space. However, the main concern is whether such privatisation will truly translate into equitable access for marginalised groups and women. To understand the Sabka Bima Sabki Raksha proposal, it is essential to first understand how the insurance sector has evolved over the years.

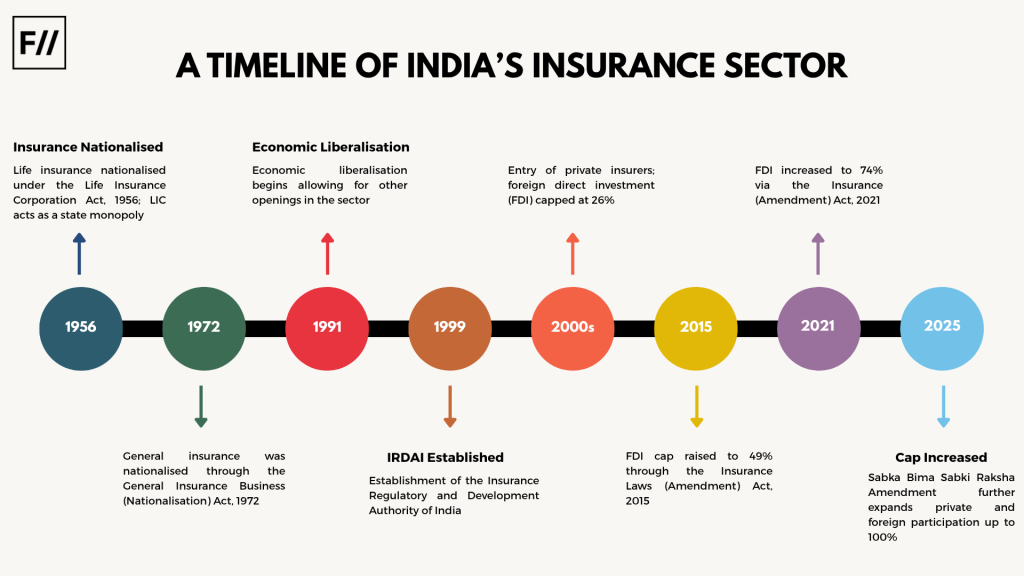

How India’s insurance sector evolved

India’s insurance industry did not aim to be a social welfare project but became one. Private players initially introduced policies, and the sector was later nationalised in the decades following independence, to align with the broader vision of social welfare schemes introduced by the Government of India. Insurance policies were envisioned as a tool to reach all socio-economic classes and not merely as a financial safeguard.

Insurance policies were envisioned as a tool to reach all socio-economic classes and not merely as a financial safeguard.

However, the reforms initiated in the 1990s marked a turning point. The rise in population and rapid developments in health care created an enormous business opportunity, leading to insurance being viewed as more than just a public obligation. With the establishment of the Insurance Regulatory and Development Authority (IRDAI), private players entered the sector. Over time, Foreign Direct Investment (FDI) caps were steadily relaxed.

The liberalisation of the economy resulted in the focus shifting to financial growth instead of social welfare. The Sabka Bima Sabki Raksha (Amendment of Insurance Laws) Act, 2025, represents the culmination of this shift: insurance coverage with a global vision and international capital in India.

Global insurance companies entering the Indian insurance ecosystem help increase capital through FDIs and foreign participation, facilitate technology transfers, and improve social security systems. Increasing digitisation has also impacted the insurance sector, with insurance claims being settled proactively, faster claim processing, easier access to purchases, customised insurance products based on affordability, and so on.

Beyond the business of insurance

Yet this narrative of progress distorts a critical reality. The business model of private insurance companies relies largely on high returns and low risk; the customer profile focus is also saturated with the urban population. This, in fact, takes us away from the underlying aim of nationalising the sector in the first place: to make insurance available for all and to make it a social welfare mechanism.

This creates a system in which healthcare advancement is disproportionately focused on the wealthy, while rural populations are excluded and neglected. As a result, they are forced to rely on public health services.

High-risk, low-income groups are left out of this equation, and the objectives of the 2025 Amendment Act are unlikely to benefit them. This creates a system in which healthcare advancement is disproportionately focused on the wealthy, while rural populations are excluded and neglected. As a result, they are forced to rely on public health services, which are still a work in progress in terms of technological advancement and adequate investment from the Government of India.

Government schemes like Ayushman Bharat (PM-JAY) try to bridge these gaps by offering subsidised health insurance to the economically marginalised. Nevertheless, these programs tend to depend on private insurance companies for execution, making the distinction between welfare and profitability hazy. Further, despite the expansion of coverage, access is not always even, especially when people don’t have adequate knowledge or leverage.

Recognition of the social nature of insurance in Indian courts has been around for some time now. The Supreme Court in the case of Life Insurance Corporation of India v. Consumer Education & Research Centre held that the right to health was an essential part of the right to life enshrined under Article 21. The Court highlighted the social role played by insurance in ensuring that the guarantees provided under the Constitution were fulfilled. The same point was made by the Supreme Court in Biman Krishna Bose v. United India Insurance Co. Ltd.

The gendered exclusion of women

This is where the gendered consequences of the new amendment emerge. Women in India are disproportionately concentrated in informal and unpaid labour. 82 per cent of working women are employed in the informal sector, according to a report by the International Labour Organisation (ILO). This structurally excludes them from employer-based health coverage, which remains tied to formal employment of 10 or more workers.

As a result, only 30 per cent of women aged 15–49 hold any form of health insurance, as per data from the National Family Health Survey (NFHS)- 5. State-backed employer-linked schemes, such as the Employee State Insurance Scheme (ESIS) or the Central Government Health Scheme (CGHS), reach as few as three to six per cent of women nationally.

The gender wage gap, with women engaged in regular job sectors making 27 per cent less than men in urban India, serves as another barrier preventing women from obtaining private insurance. Women also experience difficulties accessing care due to discrimination within the medical field and obstacles with filing claims. Further, patriarchy within homes results in women’s healthcare and health needs being overlooked in their households.

Moreover, insurance products themselves reflect and reproduce inequality. Traditional health insurance in India is designed around episodic hospitalisation, consistently missing women’s specific needs

Moreover, insurance products themselves reflect and reproduce inequality. Traditional health insurance in India is designed around episodic hospitalisation, consistently missing women’s specific needs. For instance, maternity coverage comes with two to four year waiting periods and sub-limits that fall short of actual costs, while infertility treatments and postpartum complications remain routinely excluded.

Mental health coverage is similarly inadequate, with psychological disorders historically listed as exclusions and outpatient therapy absent from most plans. Further, conditions specific to women, such as PCOS, endometriosis, and postpartum depression, remain largely uninsured, while actuarial practices translate gendered assumptions into higher premiums or restricted benefits. As foreign and private insurers gain a stronger foothold, there is a risk that these biases will be embedded within an increasingly market-driven system.

On the one hand, it would be simplistic to understand liberalisation in terms of exclusivity alone. With the growth of the insurance industry, aided by increasing foreign investment, there is the prospect of creating employment and improving financial inclusion. The involvement of women in the sale of insurance policies, online banking, and micro-insurance could very well alter gender dynamics at a more fundamental level. Yet this cannot happen automatically — it requires specific policy considerations.

The key to Sabka Bima Sabki Raksha is its universal ideal, but universality without equity may well be nothing more than window dressing. While the 2025 amendment raises the FDI ceiling to 100 per cent, it remains a gamble that foreign capital will increase penetration rates.

However, on the other hand, private insurance companies serve the middle class by design. While those employed in the informal sector — a group in which women are disproportionately represented — can only purchase insurance if heavily subsidised. Without state subsidies and gender-sensitive product mandates, any market liberalisation merely perpetuates a policy failure that has never succeeded in creating a viable business model for serving the most disadvantaged.

As India throws open its insurance industry to international investors, an interesting comparison emerges from a more balanced approach elsewhere. In Europe, private insurance serves as a complement to publicly provided services, not a substitute. In Thailand, the state-subsidised Universal Coverage Scheme includes informal labour at zero cost, whereas private insurance serves only as an additional benefit. In both cases, the state lays down the minimum, and the market enhances the maximum. In India’s case, without subsidies, gender-based requirements, and substantial state intervention, there is a real danger of completely inverting this equation.

About the author(s)

Pooja Damodaran is a legal professional specialising in international law, arbitration, and corporate legal strategy. She holds an LL.M. from Stockholm University, is pursuing her PhD, and has been a Visiting Scholar at the Lauterpacht Centre for International Law. She currently serves as Vice President (Legal) at Siechem Technologies Pvt Ltd.